One of the key messages from the 2015 Federal Budget was the need to rebalance the Assets Test to help make access to government pensions fairer. to do this, the Government proposed to increase the Assets Test thresholds and the Assets Test taper rate from 1 January 2017.

Increase in the Assets Test thresholds

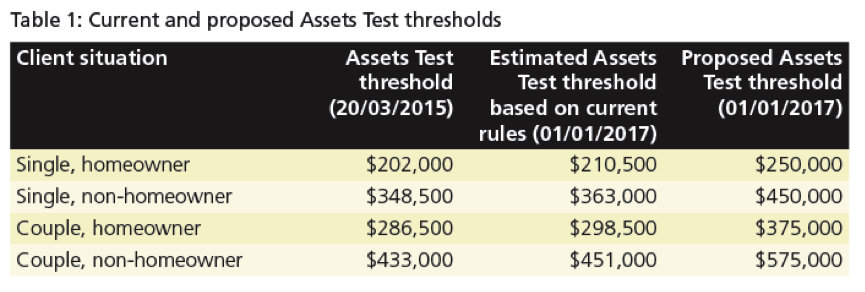

The first change to the Assets Test relates to the threshold above which a pensioner's entitlement will start to reduce. Subject to the Income Test, the proposed increase in the Assets Test thresholds from 1 January 2017 will enable approximately 50,000 part-pensioners to qualify for hte full pension under the new rules, according to the Federal Government.

The current and proposed thresholds are as follows:

Example: Ben is a 67 year old retiree who is single and owns his home. he has $10,000 in personal effects, $240,000 in an allocated pension that was created several years ago and he is currently drawing the minimum income from that pension. Based on current ruiles, he is entitled to an Age Pension of $20,943 pa under the Assets Test. If he was subject to the proposed thresholds today, he would be entitled to the full pension (currently $22,365pa)

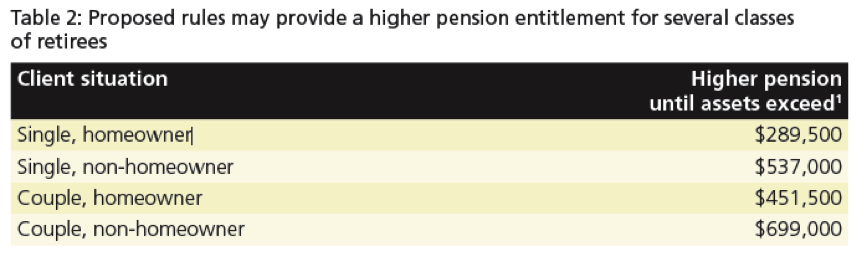

In fact, under the proposed changes, several classes of retirees may receive a higher pension entitlement.

Increase in the taper rate

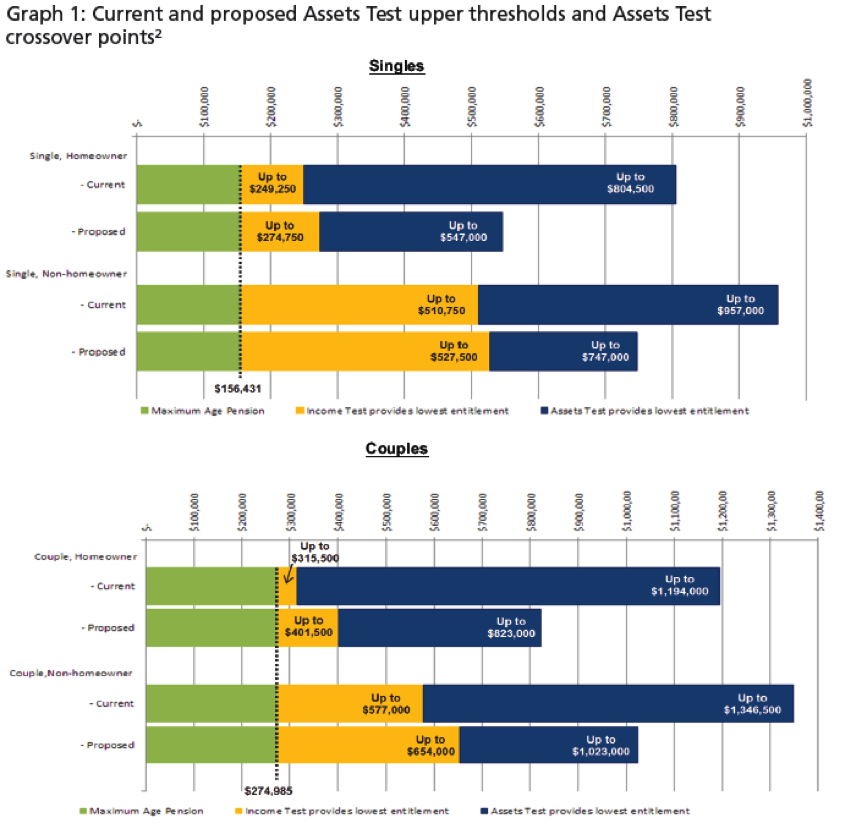

The other main proposal, which will effectivley reverse cahnges to the taper rate introduced in 2007, increases the current taper rate from $1-50 per $1,000 to $3 per $1,000. this means that the amount of assets a pensioner can have on top o their familiy home and still receive a part pension (Assets Test upper threshold) will be reduced. An estimate of the new Assets Test upper thresholds can be found in Graph 1.

The Government will ensure that anyone who is affected by the scaling back of the maximum asset threshold will be guaranteed eligibility for Commonwealth Seniors Health Card for those who are above Age Pension age or Health Care Card for those under Age Pension age. The Governmentn has not provided grandfathering for the actual Assets Test changes, so those with assets above the new Asset Test upper thresholds will lose their part-pensions and become self funded.

It is interesting to note that the higher taper rate affects homeowners more than non-homeowners and is reflected in the larger proportional drop of the Assets Test upper threshold. For example, the Assets Test upper threshold for a single homeowner reduces by about 32% compared with a single non-homeowner which reduces by 22%.

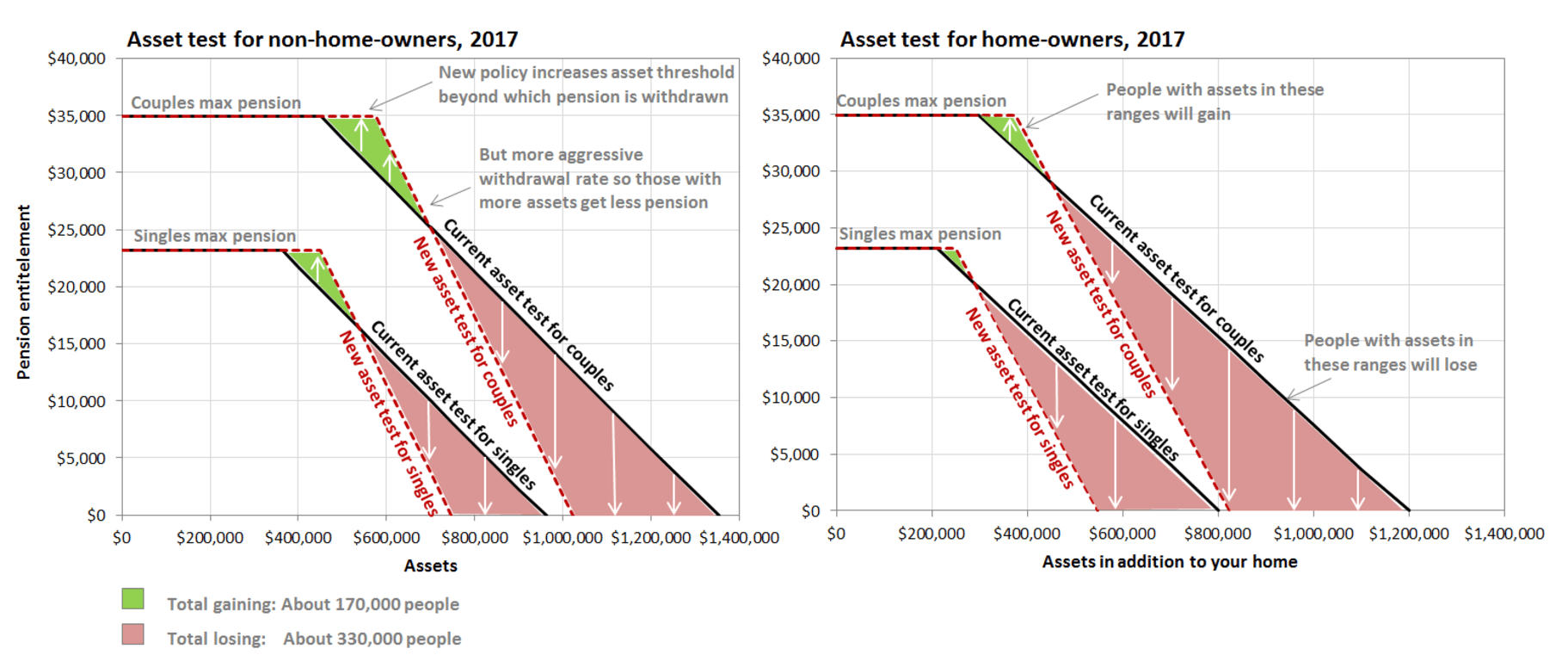

Althought the new taper rate will affect some more than others, those affected most will be pensioners with assets around the new Assets Test upper thresholds. The next chart is another way of highlighting the winners and losers from these changes. The areas highlighted in red show the the asset levels where pensions will be lower, while those areas in green indicate asset levels where the pension increases.

For example, couple homeowners will be affected the most if they have assets of $823,000 on 1 January 2017. Under the new rules, the couples pension would reduce to zero based on the Assets Test. Under the current rules, they would be entitled to Age Pension of $14,467pa. These retirees may need to withdraw more from their retirement capital to maintain their lifestyle.

Assets Test crossover points

The proposed rules will change the Assets Test crossover points. The crossover point, which assumes all assets are financial assets, highlights where a retiree's pension entitlement changes from being determined by the Income Test to being determined by the Assets Test. Graph 1 summaries the crossover points based on current and proposed rules, showing a larger change for couple retirees rather than singles.

Ways to reduce assessed assets (other than additional spending)

Those looking to reduce their assessable assets could consider the following options (in conjunction with professional advice):

1. Gifting within the allowable limits

2. Purchasing Funeral Bond

3. Superannuation contributions on behalf of a spouse under Age Pension age.

4. Capital expenditure around the home

This is a complex area and we recommend those impacted by these rule changes seek professional advice well before 1st January 2017.