![]() Summary of the Medibank Offer

Summary of the Medibank Offer

The privatisation of Medibank Private Limited (ASX: MPL), or Medibank, provides an opportunity to invest in Australia's largest private health insurer at a fair price or better, depending on the price set in the institutional bookbuild.

All considered, we recommend investors consider applying for shares in the initial public offer, or IPO, though it is not as attractively priced as we hoped. We are disappointed retail investors are only given a broad indicative pricing range before they are required to apply (which has been a feature of private-equity-sponsored issues), rather than a fixed price.

Operating in a heavily regulated industry, Australian health insurers typically produce defensive earnings. In our opinion, Medibank is well placed to produce solid long-term earnings growth from productivity improvements and industry-wide growth.

Key Takeaways

-

× We recommend investors apply for stock through the IPO. Based on Medibank's proforma accounts, guidance, business assumptions and our earnings forecasts, our fair value estimate is AUD 2.10 per share with a medium fair value uncertainty rating.

-

× The indicative price range of the IPO of AUD $1.55 to AUD $2.00 per share represents a discount to Morningstar's $2.10 fair value estimate of between 26% and 5%. Lonsec have announced a valuation of $2.33 per share. We consider Medibank attractively priced in the bottom half of the price range and roughly fairly valued at the top.

-

× Medibank looks attractive because of its strong competitive advantages, the heavily regulated industry and high entry barriers, leading to returns comfortably exceeding the firm's 10% cost of capital.

-

× Our positive view is underpinned by solid prospects for long-term earnings growth (averaging 10% per year during the next five years), low capital requirements, high returns on equity (growing to 24% by fiscal 2019), high dividend payouts (target range 70% to 80%) and relatively attractive fully franked dividends (4.3% yield for fiscal 2016 based on our valuation).

-

× Government initiatives designed to support private health insurance are the Medicare levy surcharge, the private health insurance rebate and the lifetime heath cover policy. Solid demand for private health insurance and population growth underpin our forecast 3% annual increase in policyholder numbers across the industry, with Medibank expected to lag the average for at least the medium term.

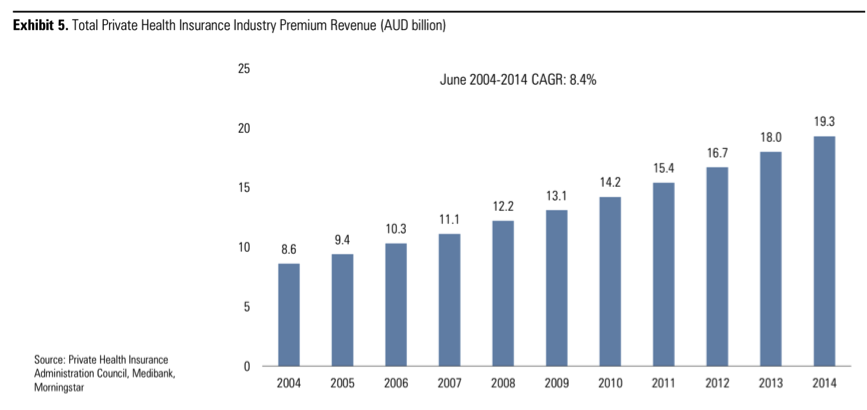

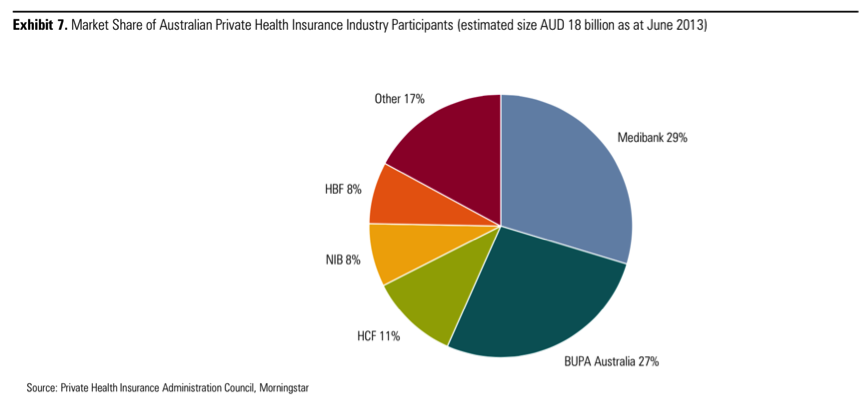

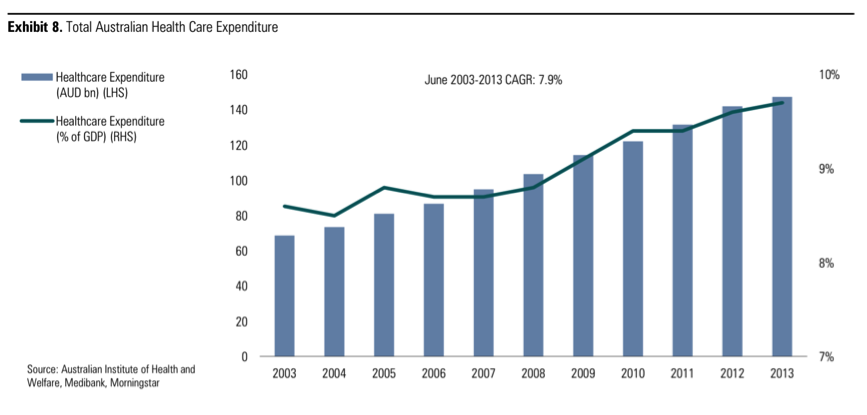

Here are a handful of useful charts that outline the attractiveness of Medibank for long term investors.

Clients of GEM Capital will receive a complete copy of this research. If you would like to receive a copy of the complete research paper please either ring (08) 8273 3222 or email

You can also obtain a PDF of the prospectus by clicking the following link Download Medibank Prospectus PDF

This information is of a general nature only and neither represents nor is intended to be personal advice on any particular matter. We strongly suggest that no person should act specifically on the basis of the information contained herein, but should obtain appropriate professional advice based upon their own personal circumstances including personal financial advice from a licensed financial adviser and legal advice. Fortnum Private Wealth Pty Ltd ABN 54 139 889 535 AFSL 357306