Summary of key proposals from Federal Budget

We can not remember a Federal Budget that has caused so much controversy in recent times. Apart from broken election promises, there has been heavy criticism of the Treasurer and Treasury Dept for a lack of consultation and a lack of depth of thought about some of the second and third order consequences of the tax changes announced in the Budget.

There have already been several back downs by the Government as a result of electorate backlash, and we would imagine that several more back downs are yet to come.

The Government has separated the Federal Budget proposals into two parts, and rushed one part through Parliament with only a two day Senate inquiry. This is in contrast to the highly consultative approaches of the Hawke / Keating Government and the Howard Government when they introduced tax reforms.

Given the confusion and subsequent changes to budget proposals, we summarise the current state of play with respect to taxation changes announced in the budget.

What has passed through Parliament already

Capital Gains Tax (CGT) — from 1 July 2027

The current system where investors pay tax on only half their capital gain (the "50% discount") will be replaced for most assets including shares and property. Instead, your cost base will be adjusted for inflation (so you only pay tax on "real" gains), but there will be a minimum 30% tax rate on any gains made from 1 July 2027 onwards.

Assets you already own will be split into two parts: gains built up before 1 July 2027 will still get the old 50% discount treatment, while gains from that date onwards will be taxed under the new system. Superannuation funds (including SMSFs) are not affected and keep their existing one-third discount.

People receiving government income support payments (Age Pension, JobSeeker, Disability Support Pension etc.) are exempt from the 30% minimum tax.

One important catch on super contributions: Making tax-deductible contributions to super to reduce your capital gains tax bill may no longer work as well as it used to — and in some cases could actually leave you worse off. This is because the 30% minimum tax applies before deductions are considered, and "top-up" tax can be triggered. Advice from a tax professional is essential before acting.

Negative Gearing — from 1 July 2027

Currently, if your investment property costs more to hold than it earns in rent, you can offset that loss against your other income (like your salary) to reduce your tax bill. From 1 July 2027, this will only be allowed for newly built residential properties.

If you bought an existing investment property before Budget night (12 May 2026), you are grandfathered — the current rules continue to apply until you sell. Properties purchased after Budget night but before 1 July 2027 can still use negative gearing until that date, after which the restrictions kick in.

Shares, commercial property and other investments are not affected — you can still negatively gear these as normal. Superannuation funds are also exempt from the negative gearing changes.

Working Australians Tax Offset

The Government will introduce a $250 Working Australians Tax Offset from the 2027–28 income year, which will provide a permanent annual tax offset to individuals earning employment or sole trader income.

The measure is intended to increase the effective tax free threshold for work-related income by nearly $1,800 to $19,985, or up to $24,985 where the Low-Income Tax Offset applies.

The proposed tax offset would represent the largest permanent increase since 2012-13 and is intended to deliver targeted cost-of-living relief, alongside the already legislated further tax cuts coming into effect for the 2027 and 2028 income years.

What is yet to be tabled in Parliament

Discretionary Trusts (Family Trusts) — from 1 July 2028

Many family businesses and wealthy individuals use discretionary (family) trusts to distribute income to lower-earning family members and reduce the overall tax bill. From 1 July 2028, the trustee will be required to pay a minimum 30% tax on trust income, with individual beneficiaries receiving a tax credit for that amount.

However, distributions to a company owned by the trust will not receive the tax credit, potentially creating double taxation. Some trusts are exempt — including super funds, fixed trusts, special disability trusts and charitable trusts. There may be an opportunity to restructure existing trusts into companies or fixed trusts over a three-year transition period.

The Government has indicated that they plan to exempt Testamentary Trusts from the changes to Trusts, but we will wait for further details.

Other Comments

The Federal Budget has already had a profound impact on Property activity, with major banks reporting a material slowdown (greater than 20%) in investor lending applications. Almost half of CBA’s home loan book comes from investment loans.

Auction clearance rates have also fallen dramatically and are back at levels not seen since the COVID pandemic. This is likely to weigh on Australian retail bank earnings, in addition to materially reducing State Governments tax take from Property Stamp Duty. We continue to be very cautious toward the Australian Banking sector.

If the Government objective was to reduce property prices, we would argue why then did they apply CGT changes to all assets?

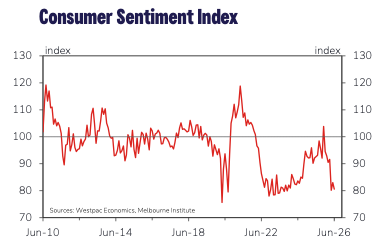

Consumer confidence was already fragile before the Federal Budget, but has since deteriorated to a level that describes consumers as deeply pessimistic. Consumer confidence is back at some of the weakest levels seen in the 50 year history of the survey. This leads us to be cautious toward investing in consumer discretionary businesses.