Key points

- The Fed’s decision not to taper reflects a desire to see stronger US economic growth and guard against uncertainties around coming US budget discussions.

- The Fed clearly remains very supportive of growth and this will help growth assets like shares, albeit there may still be a speed bump in the month ahead.

Introduction

In what has perhaps been the biggest positive policy surprise for investors this year, the US Federal Reserve decided not to start tapering its quantitative easing (QE) program and leave asset purchases at $US85bn a month. This followed four months of almost constant taper talk which had led investment markets to factor it in. As a result the decision not to taper combined with very dovish language from the Fed has seen financial markets celebrate. This note looks at the implications.

Ready, set…stop

With the Fed foreshadowing from late May, that it would start to slow its asset purchases “later this year”, financial markets had come to expect that the Fed would start tapering at its September meeting. In the event the Fed did nothing. Several factors explain the Fed’s decision:

- The Fed always indicated that tapering was conditional on the economy improving in line with its expectations whereas recent data – particularly for employment and some housing indicators – has been mixed.

- Second, the Fed has become concerned that the rapid tightening of financial conditions, mainly via higher bond yields, would slow growth.

- Third, the upcoming budget and debt ceiling negotiations (with the risk – albeit small – of a Government shutdown or technical default) and accompanying uncertainty appear to be worrying the Fed.

- Finally, the Fed may have concluded that any forward guidance it would have provided to help keep bond yields down may have lacked sufficient credibility given the coming leadership transition at the Fed.

Observing the run of somewhat mixed data lately and the back up in bond yields, I and most others concluded that the Fed would address this by announcing a small tapering, ie cutting back asset purchases by $US10bn a month, and issue dovish guidance stressing that rate hikes are a long way away in order to keep bond yields down. However, it turns out that the Fed is more concerned about the risks to the growth outlook from higher bond yields at this point than we allowed for particularly given the US budget issues.

The Fed’s announcement is ultra-dovish with tapering delayed till “possibly” later this year and the Fed further softening its guidance. For example, the mid 2014 target for ending QE is gone and the 6.5% unemployment threshold for raising interest rates has been softened with Bernanke saying rates may not be increased till unemployment is “substantially” below 6.5%. The median of Fed committee members is for the first rate hike to not occur until 2015, and for the Fed Funds rates to hit only 1% at the end of 2015 and 2% at the end of 2016.

The key message from the Fed is very supportive of growth. They won’t risk a premature tightening in financial conditions via a big bond sell off and tapering won’t commence until there is more confidence that its expectations for 3% growth in 2014 and 3.25% growth in 2015 are on track.

Given that we also see US growth picking up tapering has only been delayed, but there is considerable uncertainty as to when it will commence. The Fed’s October 29-30 meeting looks unlikely as there is no press conference afterwards and US budget concerns may not have been resolved by then. The December 17-18 meeting is possible as it is followed by a press confidence but is in the midst of holiday shopping. So it could well be that it doesn’t occur till early next year.

Perhaps the main risk for the Fed is that by not tapering (when it had seemingly convinced financial markets that it would) it has created a lack of clarity around its intentions which will keep investors guessing as to when it will commence. This will likely add to volatility around data releases and speeches by Fed officials.

The US economy and inflation

In a broad sense though, the Fed is right to maintain a dovish stance:

- Growth is on the mend thanks to improving home construction, business investment and consumer spending but it’s still far from booming and is relatively fragile as the private sector continues to cut debt ratios. This is also evident in the mixed tone of recent economic indicators with strong ISM business conditions readings but sub-par jobs growth and some softening in housing indicators on the back of a rise in mortgage rates to a still low level of around 4.6%.

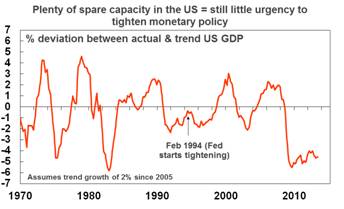

- Spare capacity is immense as evident by 7.3% official unemployment, double digit labour market underutilisation and a very wide output gap (ie the difference between actual and potential growth).

Source: Bloomberg, AMP Capital

- A fall in labour force participation has exaggerated the fall in the unemployment rate. At some point participation will start to bounce back slowing the fall in unemployment.

- Inflation is low at just 1.5%. There is absolutely no sign of the hyperinflation that the Austrian economists and gold bugs rave on about.

So while some will express annoyance that the Fed has confused them, at the end of the day the economic environment gives the Fed plenty of reason to be flexible.

Implications for investors

The Fed’s decision to delay tapering for now and its growth supportive stance is unambiguously positive for financial assets in the short term and this has been reflected in sharp falls in bond yields, gains in shares and commodity prices and a rise in currencies like the $A.

The sharp back up in bond yields since May when the Fed first mentioned tapering had left bonds very oversold and due for a rally. This could go further as market expectations for the first Fed rate hike push back out to 2015. However, the Fed has only delayed the start of tapering and as the US/global growth outlook continues to improve the upswing in bond yields is likely to resume, albeit gradually. This and the fact that bond yields are very low, eg 10 year bonds are just 2.7% in the US and just 3.9% in Australia, suggests that the current rally will be short lived and that the medium term outlook for returns from sovereign bonds remains poor.

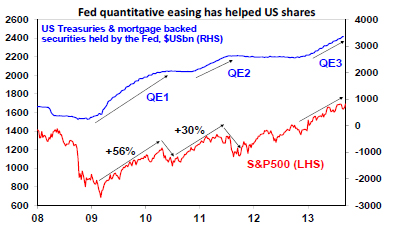

For shares, the Fed’s commitment to boosting growth is very supportive. QE is set to continue providing a boost to shares going into next year even though sometime in the next six months it’s likely to start to be wound down. But it’s now very clear that the Fed will only do this when it is confident that economic growth is on track for 3% or more and this will be positive for profits. This is very different to the arbitrary and abrupt ending of QE1 in March 2010 and QE2 in June 2011, that were associated with 15-20% share market slumps at the time. See the next chart.

Source: Bloomberg, AMP Capital

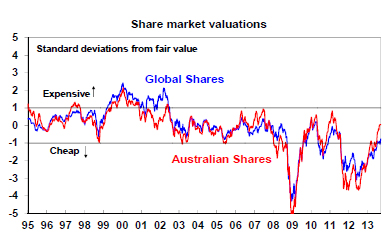

With shares no longer dirt cheap, it’s clear that the easy gains for share markets are behind us. But by the same token shares are not expensive either and an “easy” Fed adds to confidence that profit growth will pick up next year driving the next leg up in share markets.

Source: Bloomberg, AMP Capital

Shares are also likely to benefit from long term cash flows as the mountain of money that has gone into bond funds since the GFC is reversed gradually over time with some of it going into shares. See the next chart.

Source: ICI, AMP Capital

However, while the broad cyclical outlook for shares remains favourable, there will be some speed bumps along the way. The coming government funding and debt ceiling negotiations in the US could create uncertainty ahead of the usual last minute deal. And investors will now be kept guessing about when the first taper will come which means any strong economic data or hawkish comments from Fed officials could cause volatility. The May-June share market correction was all about pricing in the first taper and that process might have to commence all over again at some point.

For high yield bearing assets generally, eg bank shares, the Fed’s inaction and the rally in bonds will provide support. However, underperforming cyclical stocks, such as resources, may ultimately be more attractive as they offer better value and will benefit as the global and Australian economies pick up.

For emerging world shares, the Fed’s inaction takes away some of the short term stress, but it’s likely to return as US tapering eventually comes back into focus with current account deficit countries like India, Indonesia and Brazil remaining vulnerable.

Finally, the Fed’s decision not to taper does make life a bit harder for the Reserve Bank of Australia in the short term in trying to keep the $A down. It has added to the short covering bounce that has seen the $A rise from $US0.89 this month and so adds to the case for another interest rate cut. However, the rebound in the $A is likely to prove temporary as the Fed is expected to return to tapering some time in the next six months.

Dr Shane Oliver

Head of Investment Strategy and Chief Economist

AMP Capital

DISCLAIMER: The above information is commentary only (i.e. our general thoughts). It is not intended to be, nor should it be construed as, investment advice. To the extent permitted by law, no liability is accepted for any loss or damage as a result of any reliance on this information. Before making any investment decision you need to consider (with your financial adviser) your particular investment needs, objectives and circumstances.